0% found this document useful (0 votes)

51 viewsAssignment: Banking & Insurance

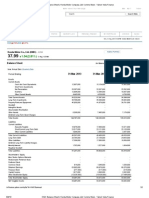

This document compares the financial performance of Punjab National Bank and HDFC Bank. It analyzes various financial indicators like profit, assets, deposits, etc. Punjab National Bank has higher profit, savings deposits, assets, branches and ATMs compared to HDFC Bank. However, HDFC Bank charges higher interest rates on loans and penalties. Both banks can improve customer satisfaction - HDFC Bank by revising interest policies and Punjab National Bank by focusing on staff behavior and improving ATM services. In conclusion, Punjab National Bank has better financial standing but both banks need work on customer service issues.

Uploaded by

Ashu GumberCopyright

© Attribution Non-Commercial (BY-NC)

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

51 viewsAssignment: Banking & Insurance

This document compares the financial performance of Punjab National Bank and HDFC Bank. It analyzes various financial indicators like profit, assets, deposits, etc. Punjab National Bank has higher profit, savings deposits, assets, branches and ATMs compared to HDFC Bank. However, HDFC Bank charges higher interest rates on loans and penalties. Both banks can improve customer satisfaction - HDFC Bank by revising interest policies and Punjab National Bank by focusing on staff behavior and improving ATM services. In conclusion, Punjab National Bank has better financial standing but both banks need work on customer service issues.

Uploaded by

Ashu GumberCopyright

© Attribution Non-Commercial (BY-NC)

Available Formats

Download as DOCX, PDF, TXT or read online on Scribd

/ 9